What is Propertyology? Propertyology – the ”science” or deep study of bricks and mortar in economic history. The real magic of a great property blog isn’t just the...

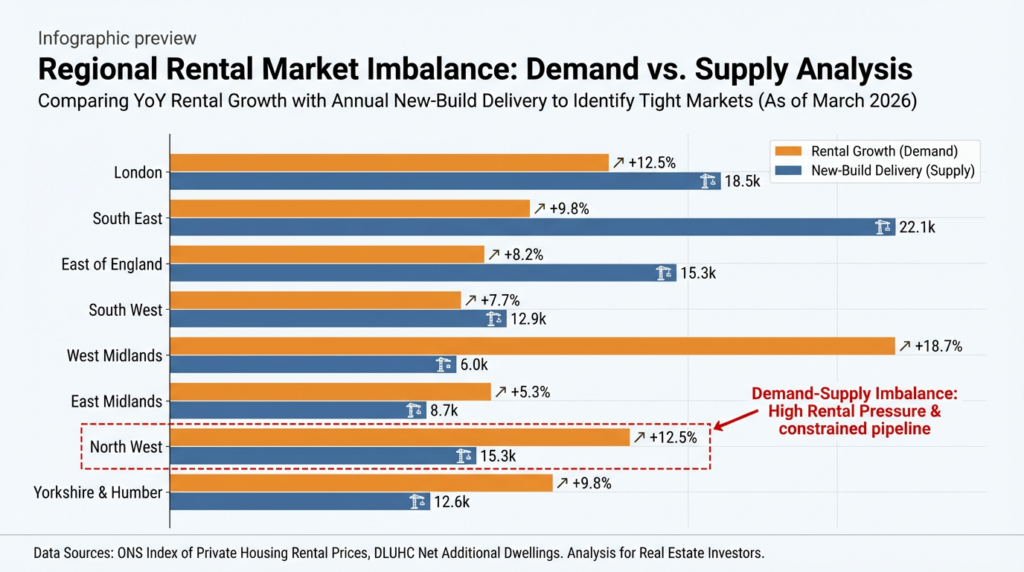

The Blueprint Advantage: A Core Guide to Rental Markets & returns The UK rental market outlook for landlords operate at the intersection of rental demand, supply constraints, mortgage costs, and...

Oxford’s 2026 Market Reset Oxford enters 2026 with a rare combination of increased housing supply, persistent structural undersupply, and record rental demand—creating a market where investors must...

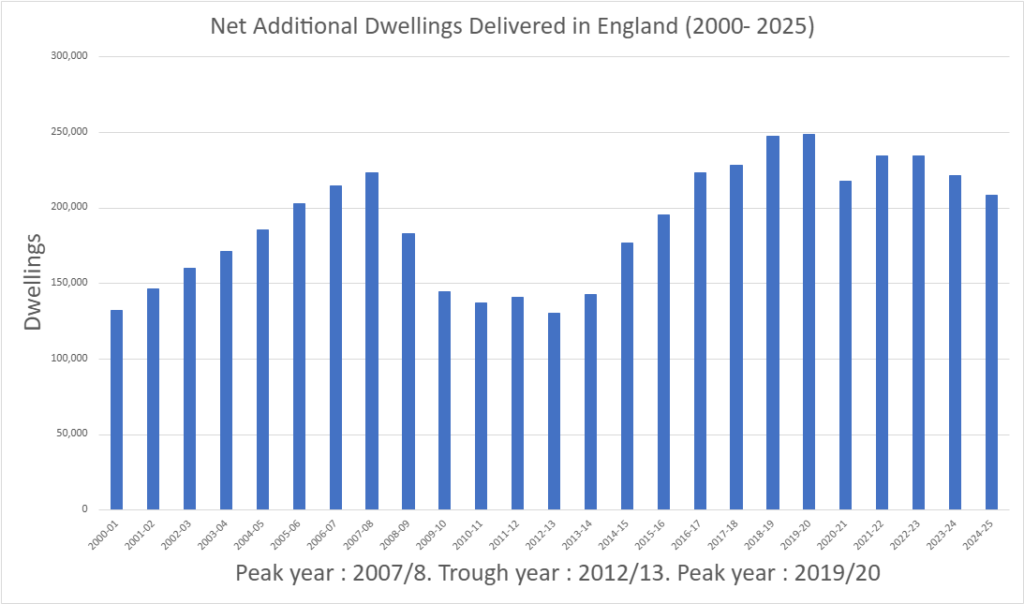

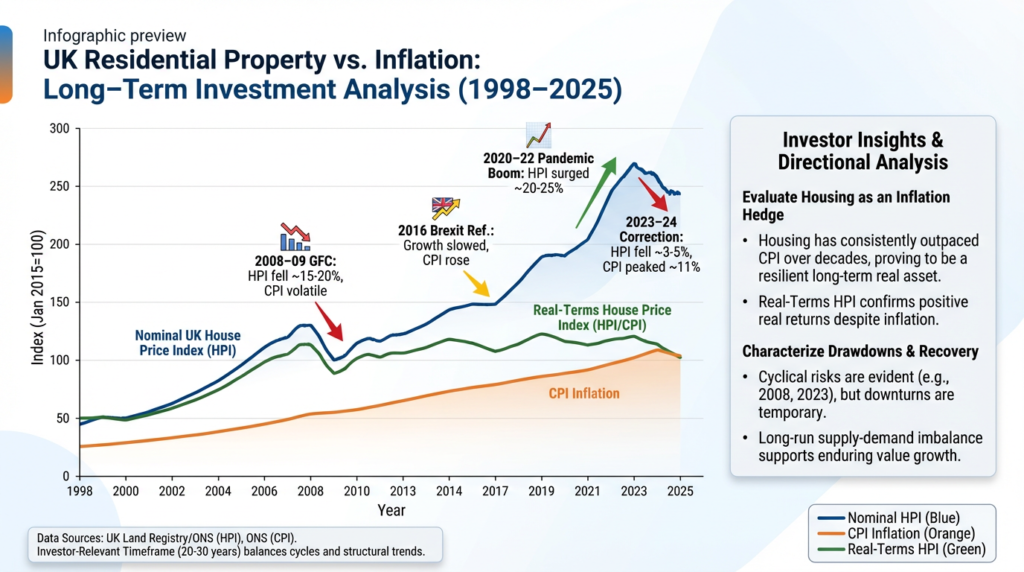

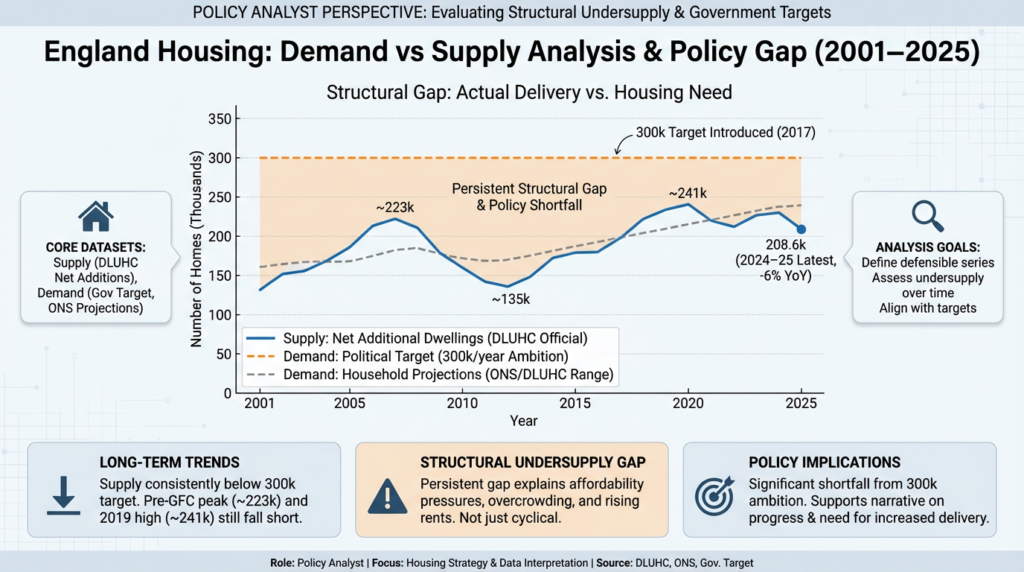

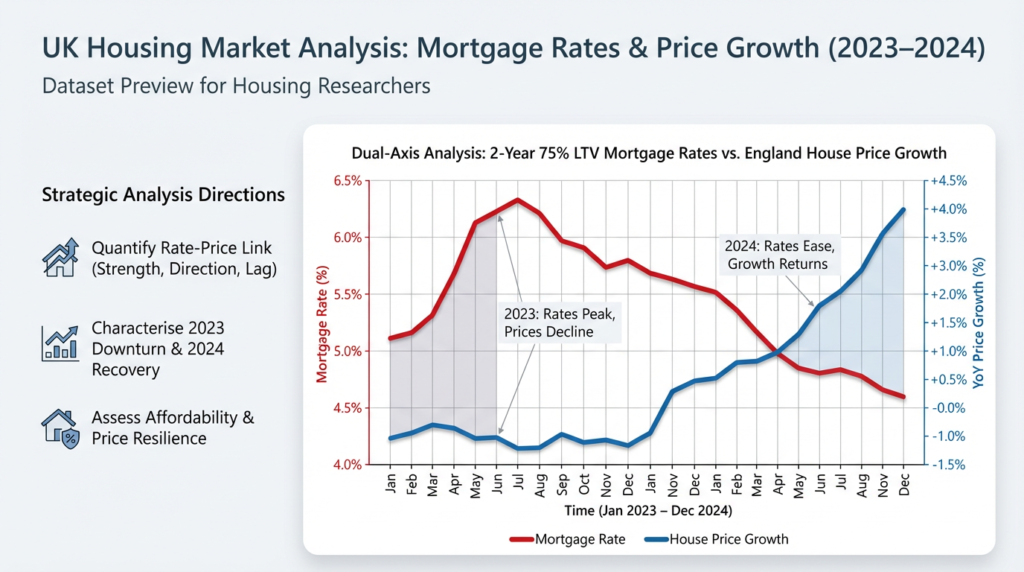

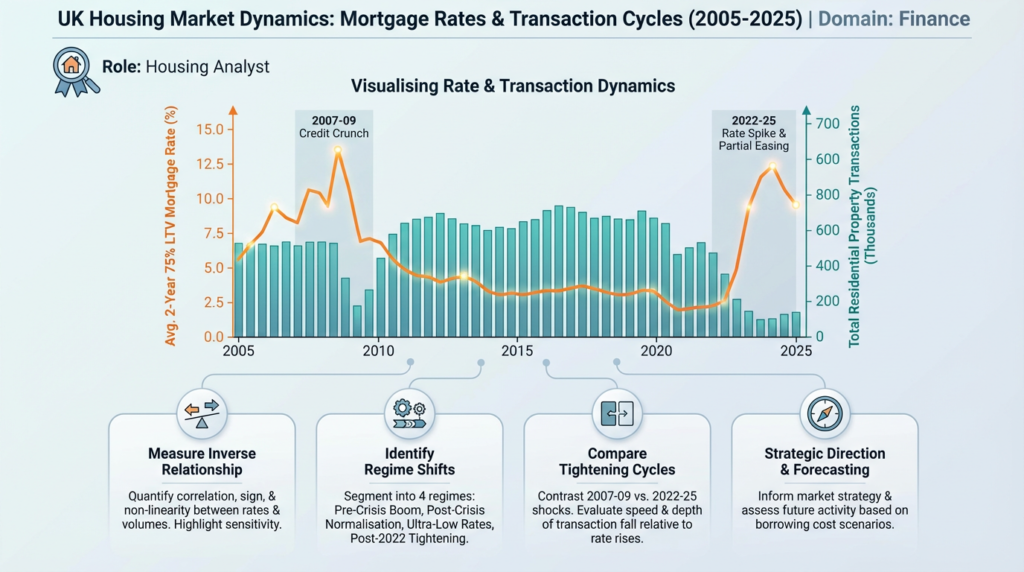

A data‑driven framework for identifying resilient markets, pricing risk, and allocating capital with confidence The UK housing market investment framework is often described as unpredictable — but for...

A strategic guide for UK homeowners who want to sell smarter, faster, and for the right price. Price right and sell fast. However, selling a home isn’t about guessing the “right” price or waiting for...

A practical, data‑driven guide for homebuyers who want to make smarter decisions in a complex market. Buying a home in the UK can feel overwhelming — headlines contradict each other, prices move...

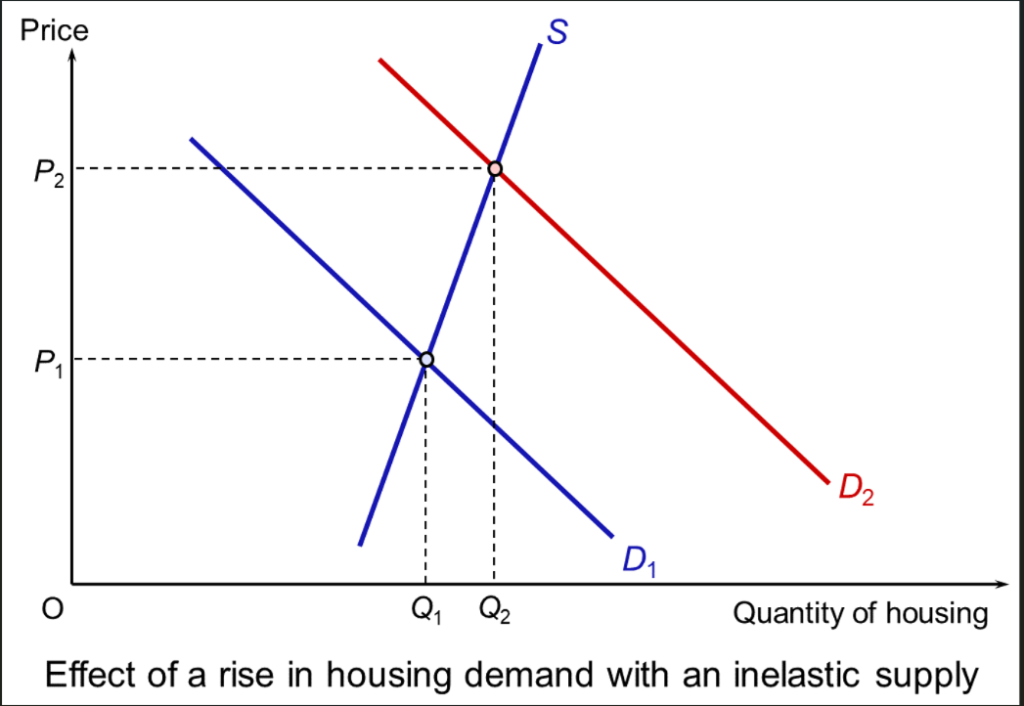

A definitive guide for buyers, sellers and investors who want to understand what really drives the UK housing market. Understanding the UK property market fundamentals and what drives price is very...

Railroads Revolutionised the Industrial Revolution Railroads reshaped property values. Railroads were one of the defining forces of the Second Industrial Revolution (c. 1880–1910). They did far more...

The Industrial Catalyst: How Infrastructure Refined UK Property Value Transport was one of the most powerful forces behind the rise of modern UK property markets. During the First Industrial...