Why a 26‑Year Supply–Demand Gap Is Reshaping Returns

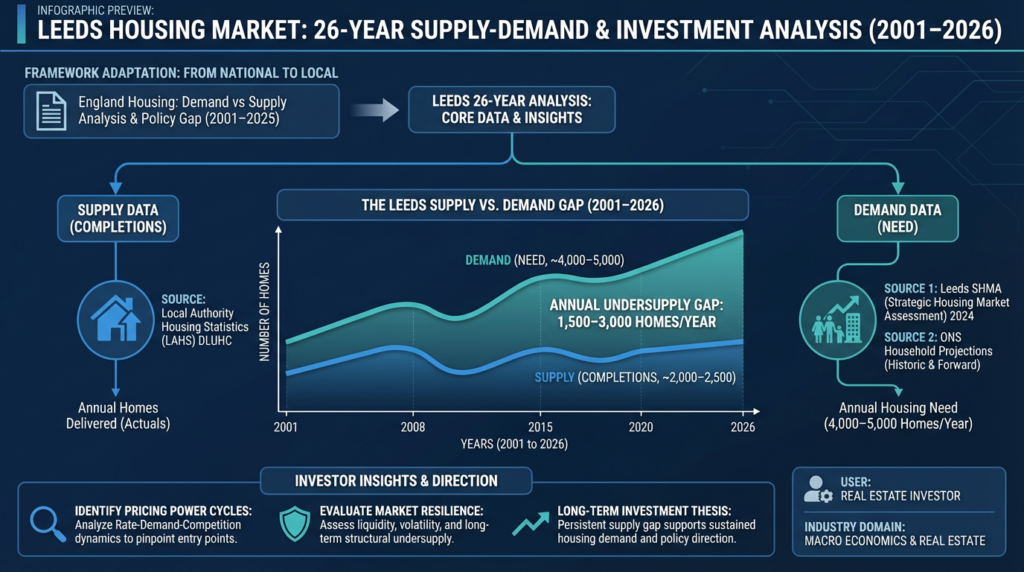

The 26‑year supply–demand gap in Leeds shows a market where housing need has consistently outpaced housing delivery, with demand running at roughly 4,000–5,000 homes per year while supply has remained closer to 2,000–2,500.For home buyers, this means competition for quality stock is intense and prices remain resilient even during national downturns.For property investors, the long‑term undersupply creates a structurally strong environment for rental growth, low void periods, and stable yields, supported by a deep tenant pool of students, young professionals, and relocating workers.For landlords, the persistent shortage reinforces pricing power, strengthens tenant demand, and reduces the risk of prolonged vacancies — especially for well‑located, energy‑efficient homes.In short, the chart confirms that Leeds’ housing market is driven by chronic scarcity, making it one of the most fundamentally resilient and opportunity‑rich cities in the UK for long‑term investment.

Key Drivers of Leeds Housing Market in 2025–2026:

- Persistent Supply-Demand Imbalance: Despite high levels of development, the demand for housing (especially family homes and affordable rentals) has outstripped supply for over two decades. Local Authority Housing Statistics (LAHS), DLUHC: Shows annual completions for Leeds over decades – consistently below assessed need. Leeds SHMA (Strategic Housing Market Assessment): Confirms long-term undersupply, affordability pressures, and unmet need. ONS Leeds Household Projections: Shows household growth outpacing new supply.

- Strong Price Growth (2025–2026): As of early 2026, the average house price in Leeds was approximately £246,000, marking an annual rise of 4.1% compared to January 2025. This outperformed the broader Yorkshire and The Humber region (3.0%).

- Rental Market Surge: Average monthly rents in Leeds are hovering around £1,100–£1,126, having increased by roughly 25%–30% since 2020, driven by population growth and high retention of graduates.

- Record Construction vs. Continued Need: In the year to March 2024, nearly 4,500 new homes were built, a potential 40-year high. However, council officials noted that this, “significant” development is still insufficient to meet the rapidly rising population’s needs.

- Strategic Undersupply Areas: There is a specific, chronic shortage of affordable rental stock (LHA rate) and 2-3 bedroom family homes.

- Market Resilience: Despite higher interest rates, Leeds’ market remained robust due to limited stock, with 2026 forecasts suggesting continued, though perhaps slower, price growth.

Why Leeds Still Attracts Property Investors

Leeds has quietly evolved into one of the UK’s most resilient regional cities. Key reasons for continued investment in Leeds include:

- Exceptional Rental Demand & Yields: A booming rental market, supported by over 80,000 students and a large young professional population, provides consistent rental income. Some areas generate rental yields up to 10.6%.

- High Capital Growth Potential: Property prices in Leeds are forecast to increase by over 20% by 2028. With prices having increased by around 25% over the last five years, it remains a strong market for capital appreciation.

- Major Regeneration & Infrastructure: Key projects like the South Bank development, Victoria Gate, and improvements to Leeds Bradford Airport are increasing the city’s desirability.

- Affordability vs. Growth: Despite rising prices, Leeds offers better value compared to southern cities, with average prices sitting below the UK national average {~£268,000}, attracting first-time and experienced investors.

- Diverse Economy & High Employment: As a major financial, legal, and digital hub, the city offers stable employment, driving consistent rental demand.

- Strategic Connectivity: Excellent transport links, including a 2-hour rail link to London, make it a key commuter and business location.

The city’s rapid population growth ensures that demand for housing continues to outstrip supply, solidifying its status as a top northern investment location.

Investing in Leeds: High-Yield Hotspots vs. Capital Growth Hubs

Leeds continues to be a powerhouse for Buy-to-Let investors, offering a distinct split between immediate rental income and long-term equity growth. To maximize your ROI, your choice of postcode should align strictly with your financial strategy.

High-Yield Districts: The Cash Flow Kings

For investors prioritizing monthly “net” income, the city centre and inner-city suburbs dominate. These areas are fuelled by a massive student population and a thriving young professional demographic.

- LS2 (City Centre): One of Leeds’ strongest rental yield zones, typically 6–7%, with upper‑bound cases reaching 8–9% in select blocks. High demand from students and professionals keeps void periods among the lowest in the city, especially in modern build‑to‑rent and luxury schemes.

- LS2 (Quarry Hill / SOYO): A regeneration‑driven district delivering 7–9% yields, particularly in Harehills and the eastern LS9 corridor. Major cultural, residential, and infrastructure projects around SOYO and Quarry Hill continue to strengthen long‑term rental demand.

- LS3 (Burley / City Fringe): Close to both universities and the city centre. Standard rentals deliver 5–6%, with HMOs reaching 7–9% depending on layout and licensing.

- LS4 (Burley & Kirkstall): A strong rental district driven by students and young professionals. Typical yields sit around 5–6%, while well‑configured HMOs can achieve 8–10%.

- LS6 (Headingley / Hyde Park): The heart of Leeds’ student market. HMO conversions typically achieve 7–10% yields, depending on configuration and licensing. Standard single‑lets in these postcodes sit lower (around 4.5–5.5%), but HMOs remain the top performer for cash‑flow‑focused investors.

- LS11 (Beeston/Holbeck): Consistently among the highest‑yielding postcodes, averaging 7–8%, with some streets exceeding this. Regeneration around Holbeck and the South Bank continues to support above‑average rental demand.

Investor Tip:

When targeting the high-yield areas, ensure you are up to

date on Leeds City Council’s Article 4 Directions, which

impact HMO planning permissions.

Selective Licensing: As of February 9, 2026, parts of

Armley, Beeston, and Harehills require a license even if

it’s not a large HMO.

Capital Appreciation Hubs: The Long-Game Plays

While these postcodes show lower rental yields (typically 3–4%), they are premium locations. Investors here trade monthly cash flow for stability, high-quality tenants, and significant long-term capital gains.

LS16 & LS17 (Adel/Bramhope & Alwoodley/Moortown): These are Leeds’ “Gold Coast” suburbs. With yields averaging 3.4–3.6%, the value lies in the prestigious addresses and historical price resilience.

LS8 (Roundhay/Oakwood/Harehills): Mirroring the Roundhay market, this area attracts families and affluent professionals, offering a stable but lower yield of ~3.7%.

LS15 (Temple Newsam): A popular residential choice where high entry prices result in a modest 3.8% yield, compensated by strong demand for family homes.

Investor Summary

| Strategy | Target Postcodes | Typical Yield | Key Driver |

| High Income | LS2, LS3, LS4, LS6, LS11 | 7% – 10% (HMOs) | Student/Pro demand |

| Capital Growth | LS16, LS17, LS8, LS15 | 3% – 4% | Premium lifestyle |

Not investing in Leeds?

Get the 2026 Outlook for your specific target city.

Register your interest here